Remember when Malcolm Turnbull, the goddamned idiot who was briefly

Prime Minister of Australia, was told that the laws of mathematics mean

that there was no way to make a cryptography system that was weak enough

that the cops could use to spy on bad guys, but strong enough that the

bad guys couldn’t use it to spy on cops, and he said:

“Well the laws of Australia prevail in Australia, I can assure you of

that. The laws of mathematics are very commendable, but the only law

that applies in Australia is the law of Australia.”

He added: “I’m not a cryptographer, but what we are seeking to do is to

secure their assistance. They have to face up to their responsibility.

They can’t just wash their hands of it and say it’s got nothing to do

with them.”

Malcolm Turnbull lost his job, though not for saying this goddamned

idiotic thing. This goddamned idiotic thing has continued to fester in

Australian politics, until today, when the pustule ruptured and

Parliament sat down and voted to make the laws of Australia prevail over

the laws of mathematics.

Good luck with that.

Under the new rule, cops can get court orders that will require tech

companies to backdoor their encryption, serve malware, or do whatever

else it takes to decrypt subjects’ messages, even if those messages are

so well encrypted that it would take more computational cycles than can

be wrung out of all the matter in the universe to brute-force the key.

Bad guys, meanwhile, can just use free/open source software, or tools

that are made by companies located outside of Australia, or tools that

exist today without any backdoors, and never fear police interception.

Making this bill work would mean a raft of extreme measures:

seizing and altering every general purpose computer in Australia;

banning the importation of any computing device, including phones and

laptops, into Australia; blocking Github and every other software

distribution site at the national level, and more.

Apropos of nothing, a little history lesson: PGP, Pretty Good Protection, was Kinda A Big Deal when it first showed up. It was a relatively simple cryptography app, readily available at the consumer level, that was mathematically provably secure – that is, it would be literally impossible to break it using the technology of its era, at least while you were still alive to worry about it.

Shortly after it hit the scene, it came out that PGP included an algorithm from RSA Security, a major American information security firm. They reported Zimmermann (the PGP guy) to the US government, who investigated him for munitions trafficking.

See, it turns out that there was a law against exporting security the US government couldn’t crack, PGP was way beyond that limit, and suddenly people were getting good security overseas. (I once heard a story involving a payphone and an analog coupler and an overseas call to a dissident group in the middle east, but I have zero evidence for it.)

They investigated Phil Zimmermann for years. For bringing security from government surveillance to the masses. Thirty years ago, they saw where this was headed.

Finally, in 1995, Zimmermann published a copy of the PGP source code in a hardback book. As it turns out, books are (or were, I don’t know if they changed this) completely legal to export. And completely possible to chop the covers and spine off of and feed to an OCR reader.

The government dropped its investigation without comment or charges in 1996.

PGP has since been bought out and handed off repeatedly, and last I heard was basically completely broken in its core use. Phil Zimmermann is part of the Dark Mail Alliance, a group working on a tool to replace PGP in the modern era, handling metadata and other things the original tool was never designed for.

There are, however, other free, open source (and thus verifiably secure – this is important!) tools in existence today, that are secure against all known practical attacks.

I’d suggest you look into this, should you have reason to think that people with power would be less than friendly to you. (I know I have to.)

After all, these tools might not be around forever.

Thank you to those of you who’ve contacted me about posts being marked as “inappropriate”.

Some of the things Tumblr has marked as inappropriate that were blogged here are as follows:

I have been going through old posts and appealing each that was improperly flagged but I think a contingency plan may be necessary. Currently I’m looking at exporting the blog to WordPress, but I’ve also considered Twitter and Facebook.

So I’m looking to you for your opinion on what would work best. Please comment or drop a note and let me know your thoughts.

Until I can no longer operate this blog, I will continue to post as much as possible and to contest this utterly incomprehensible scorched earth policy Tumblr has enacted.

All we have are our voices. They can’t silence us. They can’t take that from us.

-Spider

So much for still allowing discussions of politics, breastfeeding, etc, huh @staff?

Politics, brestfeeding, art, and just generally anything that has to do woth women’s bodies…

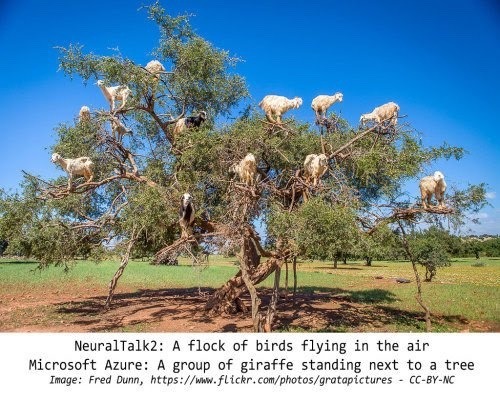

For example, image recognition has a tendency to misindentify rocky fields as goats (because goats are often found there), images with rulers are more likely to contain skin cancer, annnnnd apparently anything significantly skin toned as porn.

( #send dunes)

Not only that, but nets that were pretty good at recognizing goats regularly misIDed them when they turned up in unusual places– goats in trees = birds, goats in cars = dogs

so it’s open enrollment time, which means you need to pick a health insurance plan from the exchanges! it can be daunting as shit, for sure, especially if you don’t live in the filthy weeds that are the business side of our garbage health care industry like yours truly does.

so! here’s a quick rundown of some of the vocabulary:

premiums: this is what you pay per month for the glorious honor of having insurance coverage. it does not count towards your deductible or out of pocket maximum. depending on your income, you may be eligible for a subsidy or other financial assistance to make your premiums more affordable.

deductible: this is how much in health care costs you have to pay before your insurance starts really kicking in. for example, my insurance through work had a $1,500 deductible, so the copays and coinsurances and lab costs that i had to pay early in the year, before i had another surgery, were fully my responsibility until i’d paid out $1,500; after that, my insurance started covering a flat 80% of everything, including copays. basically, the deductible is how many actual dollars you have to pay out for medical costs before your insurance takes over.

if you’re someone who goes to the doctor a lot, like me, you’re probably going to want a plan with a lower deductible, which will have a higher premium; however, in the long run, you’ll come out more ahead with a high premium/lower deductible.

on the flip side, if you’re generally healthy and just need an annual checkup, flu shot, ob-gyn annual, etc., then you probably want a lower premium/higher deductible plan.

out of pocket maximum: this is the cap on how much– aside from premiums– you should have to pay in health care costs in a year. most plans on the exchanges right now have a high deductible and higher OOP max.

network: this is the collection of providers (doctors, surgeons, urgent care facilities, imaging facilities, etc.– any clinical medical care or medical service provider) that are contracted with the insurance plan. this means that they have an agreement with the plan to accept payment from that plan for services. you can still see out of network providers, but your plan may have a separate out of network deductible that is higher and that you pay separately from your main deductible (for example, if your plan deductible if $5,000, you might have a separate out of network deductible of $5,500; even if you’ve already paid of $4,950 of your regular deductible, if you see an out of network doctor, you’re going to have to hit the $5,500 deductible in copays and whatnot before the insurance covers them fully).

most insurers have their own website that identifies what doctors are in network. sometimes you can access this without being on the plan already, sometimes you can’t. a decent, though inconsistent, workaround is to use zocdoc, where you can put in the plan type you’re thinking about switching to and see what doctors are in network. the drawback to zocdoc is that contract status is doctor-reported, so if the doctor’s office in question is slow to update, the records may be out of date.

another option to determine network availability for a specific doctor or care group is, if you’re okay hopping on the phone, to just give them a call and ask outright if they’re going to be in network for plan ___ in 2018.

if you’re like me and hate talking on the phone, the other option is that large provider groups, and a good number of smaller groups and individual providers, will often also have accepted insurances on their websites. in my experience almost all providers who have privileges at a hospital will have that listed on their pages on the hospital’s website.

copay: this is a flat fee you pay to a provider when you see them. it’s like the cover charge at a bar: you pay $20 to get in the door, and then you get the dubious honor of also paying for the drinks and food you buy inside on top of that.

coinsurance: this is a percentage charge for seeing a provider. instead of a $20 copay for the cost of the visit to see doctor bob, you’re charged, say, 10% of the total cost of all charges associated with you visit to see doctor bob. if you don’t get much done, this may only like $10; if you get a full metabolic panel run and a bunch of xrays, it might be $100.

and the plan types:

hmo: health management organization. the concept of this plan is that you have a pcp (primary care provider – your regular doctor) who functions as your primary point of contact for all medical care. if you want to see a non-pcp doctor, you have to first see your pcp, who will write you a referral to see said specialist. specialists include orthopedists, physical therapists, neurologists, ob-gyns, etc. – any provider who isn’t your pcp, basically.

hmos tend to be cheaper for you, the beneficiary

this is because of how they’re paid out: pcp doctors receive a capitation (aka, a set flat amount) payment from the insurer for each beneficiary (you) who has them as a pcp.

so, if i’m a primary care doc and i have 200 blue cross hmo patients and i get $100 per patient, i get $20,000 from blue cross, ostensibly for the cost of care provided, but the provider keeps all $20,000 even if they only end up incurring $15,000 in costs. the downside of this for you as a patient is that this encourages pcps to get a lot of people to sign up as their patients, and then to see them as little as possible/push them out to specialists for actual care, as this lowers their costs and increases their revenues.

you may end up feeling like you’re going in circles trying to get actual care because you’re getting pushed from one doctor to another.

note: hmo plans sometimes do not cover out of network providers at all.

ppo: preferred provider organization. this plan is a free for all: if they’re in network, you can go to whomever you want. they tend to be a bit pricier (almost always on premiums, 50/50 on deductibles) than hmo plans, but you’re basically paying for ease of access. you can make an appointment directly with any specialist you so choose. these plans are ideal for people like me, since i have to see orthopedists and hematologists and physical therapists pretty regularly, and going through a pcp for each of those would be a pain.

you’ll tend to have relatively low copays within the network and higher ones outside of it

unlike some hmo plans, most ppo plans will provide coverage for out of network providers, just at a less favorable rate

epo: exclusive provider organization. this is the bastard child of the hmo and ppo and is also an increasingly common option on most of the exchanges. like a ppo, no pcp or referrals are provided; however, the network tends to be narrower and you have less choice of in-network providers and, crucially, they don’t tend to cover any out of network providers except for emergencies

important note: the classification of “emergency” isn’t just “emergency situation”, but generally is limited to a proven medical emergency in which you go to an actual emergency room or emergency department.

insurers will frequently challenge ER/ED bills to confirm medical necessity because–

in their defense, since they’re meant to cover almost the entirety of emergency bills and also because one of the quantifiable measures of success in moving to value-based care that the ACA established is lowering avoidable ER/ED admissions

–they don’t want to encourage people to go the ER/ED for just anything

high deductible/catastrophic: these are exactly what they sound like– plans for healthy young people who are pretty much only going to wind up with medical costs if something terrible and, well, catastrophic, like a car accident, happens. they have low premiums and very high deductibles (often approaching ~$10,000). these are only available to people under the age of thirty, because clearly as soon as you turn thirty you must turn into a total drain on all healthcare resources 😐

so what does all of this boil down to for you and your enrollment?

start by figuring out what financial help you’re eligible for! the exchanges generally have an option at the front end of the process for you to identify your annual income and number of dependents on your plan. this will let you know if you’re eligible for a subsidy or other financial help, and, if so, how much; you should also have an option when searching through plans on the exchanges to input estimated financial help, which will adjust the premiums in the search engine.

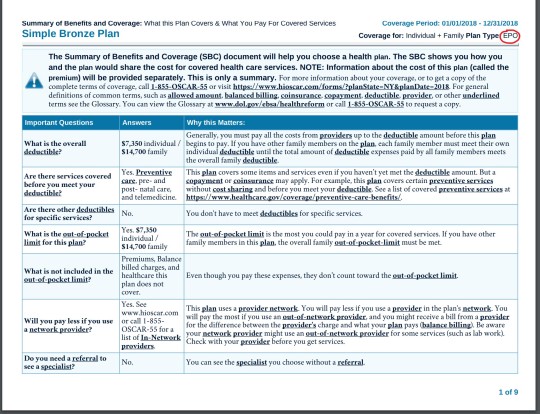

after that, start digging into the individual plan options. every exchange plan should provide a summary of benefits and coverage. it’ll be a pdf and will look like this:

that red circle in the top right there? that’s where you can identify what type of plan you’re looking at. the first page in the summary of benefits will always look the same– it’s the basic overview of the costs and definitions.

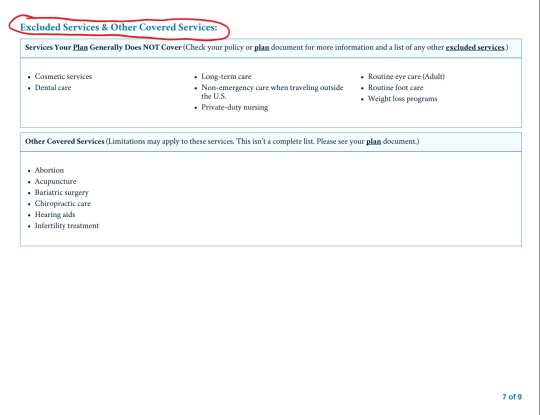

this document will also list excluded services. it’ll generally be somewhere in the middle/back half of the document and will have a clear header like this:

for me, this is the first thing i look for after verifying premium and deductible amounts. as the above picture indicates, you can find more information in the plan documents. these aren’t always directly linked to on the exchange website, but you can generally find them on the insurance providers website. these will be a lot more detailed and can be anywhere between twenty and 200 pages. ctrl + f your heart out: as frustrating and complicated as insurers can be, they can’t actually fail to disclose if they, for example, don’t cover all forms of contraceptives. they’ll disclose it in the plan documents, even if they don’t, unfortunately, have to be clear and up front about it.

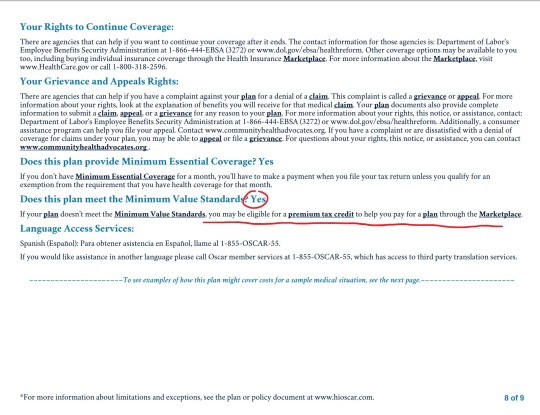

NOTE: MINIMUM VALUE STANDARDS

towards the end of the summary of benefits document will be a page that looks like this:

minimum value standards roughs out to basically meaning that at least 60% of all medical charges are covered. if the plan you’re on does not meet minimum value standards, you might be able to get a tax credit to help you buy another marketplace plan. always check for this verification when you’re researching plans.

what does all of this shit mean?

it means start here and then find your state’s exchange from there. the garbage carrot in chief established “maintenance times” on this website throughout the open enrollment period (sunday afternoons, i believe), so schedule around that. sit down on a monday or wednesday or saturday with some snacks and a cup of your favorite beer/wine/tea/whathaveyou and crank up some good music to jam to and do some research:

start with figuring out what you can afford monthly and if something terrible happens and you have to cover ER and/or surgery bills

if you have a specific doctor you want to stay with, figure out which insurances they’ll be accepting

check for coverage info in the summary of benefits documents and, if you want more detail, in the plan documents

narrow it down to a few and compare the prices

take a break and have a cookie, you deserve it at this point

pick a plan! if you’re not feeling super certain about it, go for a walk, do some laundry, pet your cat– just take a break, walk away, come back to it with fresh eyes. this is a big deal, so you don’t want to wear your brain out and give yourself a headache and then just pick one at random because you have eye strain and want to be done. open enrollment goes until december 15, so don’t rush yourself.

sign up for your plan

have another cookie and pat yourself on the back, because you just signed up for health insurance for 2018!

now take a nap because that was fucking exhausting and you deserve it

if i don’t know the answer, i can point you towards someone or some resource that will. don’t be afraid to ask me or anyone else for help! this is a complicated situation and even though the current administration is trying really hard to make it worse, there are still always resources available to you for help and guidance. all you have to do is ask 🙂

Amazon is the fucking evil megacorporation from every near-future cyberpunk story they have warehouses full of wage slaves that can’t even take a piss or fall behind their ridiculous expectations without getting fired on the spot while their CEO is nearing trillionare status day by day while quite literally making local governments pay them to determine which city they install their next slave warehouse in and now their wiretap HAL 9000 bots that are in millions of houses all over the country are doing evil laughs and reading off names of cemeteries and funeral homes completely unprompted I know anger at amazon in general is very outrage-of-the-day basic entry level american leftist reaction but Jesus fucking Christ people

Boost: Open remote job offer for disabled web page designer

WordPress based because I can’t manage anything more complex because I’m a dummy. You will require some coding knowledge because already tried the templates and still not satisfied but I don’t know how to move things or add widgets and shit

And yes I’m doing this because I’ve poured 5 years of my life here and im I’m terrified by the tumblr ban.

Having a disability (yes, mental illness counts as well) is a hard requirement because we need the jobs right?

Unemployed peers, house bound fellas or those with medical debts will be considered particularly. But you do have to do a great job.

Yes, you will be paid decently, as you should be, you’ll just need a PayPal account. You will be working for me directly. I’ll gladly provide you the information you need.

Please send your resume (it doesn’t matter if you don’t have a lot of experience as long as you do a killer job) and portfolio (I wanna see your work) to antinormal.net@gmail.com with copy to diversidadcolectivamx@gmail.com.

Don’t bother much about the cover letter, I just need the resume and a good portfolio.

If you pass the first round according to your type of work we’ll have a Skype interview on phase two.

Here’s my info again for anyone who wants to keep in touch in case my blog gets deleted. I have no way of telling if it will be or not, afaik. I intend to stick around here for now, if they let me.

mastodon: @potatoshoe@mastodon.social (how do you link to a mastodon account? I don’t know!)

I don’t use either of these very much but I’m probably going to start using them more, especially if my blog gets deleted or if enough people leave that this place stops being interesting.

If you want to keep in touch otherwise, I’d be willing to give out my email over DM as long as we’ve interacted before.

I’m trying to back up this blog to wordpress but it doesn’t seem to be working.

Repeat after me: – Veganism is not affordable – Veganism is not cruelty free – Veganism is not the best choice for everyone

Repeat after me -I’m an idiot and wrong. -Veganism can be made affordable. –Veganism is fucking cruelty free. That’s what it’s all about. – Veganism is the best choice for everyone, if everyone did it. -I’m a fucking asshole for making this completely wrong text post and should shut the hell up now.

People are literally starving in South America because all the Quinoa crop is being exported mainly for white vegans who want to live “cruelty-free” but don’t care about brown people as much as they do about animals.

plus, 4 of the 8 most common food allergies (soy, wheat, peanuts, and tree nuts) are common vegan substitutes.